The Big 12 Calls on J.G. Wentworth

Those opera bus commercials with the catchy jingle may hook the Big 12.

The choice between recurring payments versus a lump sum payment is commonly discussed with mega-million lottery prizes. The published prize amounts are typically paid out over several decades without adjustments for inflation, but the prize winner can opt to take a substantially smaller amount in a single payment.

It’s my money, I need it now!

Recent reports have the Big 12 exploring an opportunity to obtain nearly $1.0 billion in exchange for 20% of future conference and college football playoff media contract revenue. This is the same deal structure offered by JG Wentworth, the financial institution with the catchy jingle. J.G. Wentworth caters to individuals and businesses that want to convert a future stream of guaranteed payments into an immediate single payment.

The Big 12’s financial suitor is a private firm registered in Luxembourg. Beat reporters who typically deal with breaking down offenses and defenses regurgitated a few snippets of information on the potential deal without analysis. Here I try to provide context and analysis.

Borrowing money to invest is inherently risky. The risk associated with this strategy is directly related to the interest rate charged by the borrower. The higher the interest rate, the higher the risk. Borrowing money at 4%, to invest in a revenue-generating business that might yield a 10% return could make sense. Borrowing at credit card/loan shark rates never makes sense.

Based on the limited information provided to the beat reporters, I estimate the effective interest rate on the proposed advance of nearly $1.0 billion to come in at around 17%. At that rate, the winners in the deal are 1) the JG Wentworth-type lender making the “investment,” and 2) the brokers that hooked the Big 12 (brokerage fees on these deals can reach as high as 5%).

Is this private equity?

The discussion around private equity and college athletics is beyond sprawling and disjointed. There is no common understanding of what constitutes private equity, coupled with a frantic quest by athletic directors and conference commissioners to generate more money to maintain a mythical competitive balance. It is a perfect scenario for vulture equity firms to claim a victim somewhere amongst the hundreds of programs across the country.

The instrument suggested for the Big 12 is one of hundreds used by firms that make a business of providing money to others in one form or the other. It appears to be a rather simple structure, one I would label a “participating loan.” That is, the instrument has some characteristics of a loan, and some characteristics of a limited investment (i.e., one without any management control).

A straight loan would require the Big 12 to guarantee repayment of the principal amount ($960 million) with interest. Here, the only guaranteed repayments are the revenues associated with current media contracts. The Big 12 would be obligated to share those revenues - which would likely repay the amount advanced by the financier. Once the existing media contracts expire in six or so years, repayment is based on a percentage of new contracts. This second part of the deal appears to be a limited partnership, with the financier waiting passively for payment on their 20% cut. With their advance of $960 million already repaid, all of these payments, post the current contracts, are what generate a return for the financier.

The contract needs a termination date, so for purposes of this analysis, I’m choosing 20 years as the length of the contract. Revenue beyond 20 years, when taking into account the time value of money, has little impact on investor returns.

How much is the Big 12 paying for this advance?

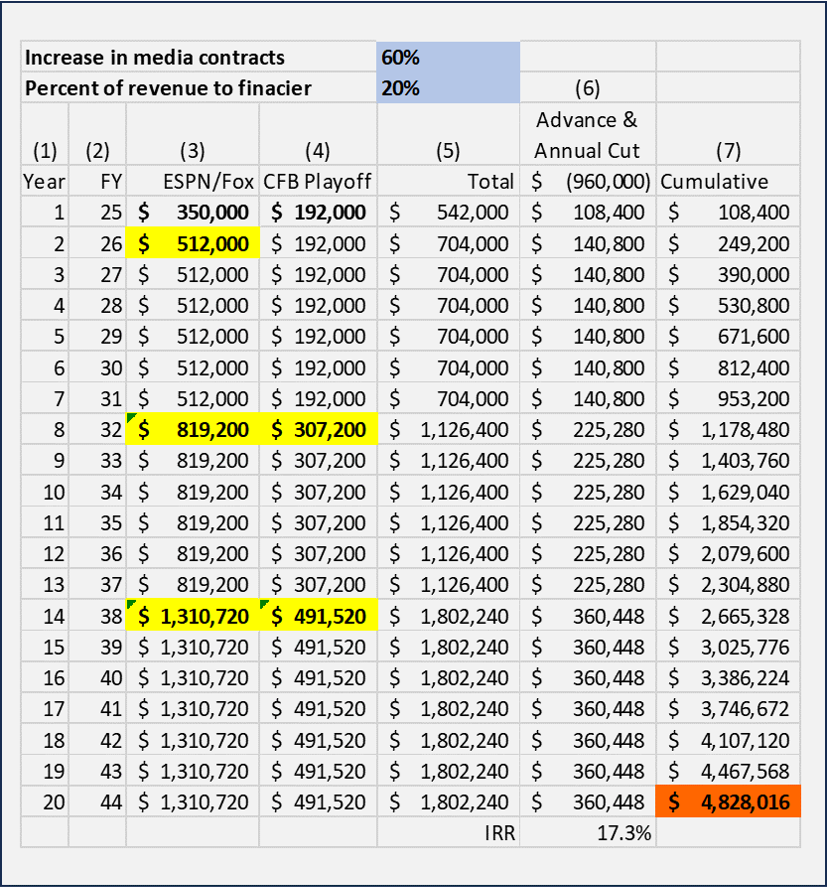

Table 1 below is a simple spreadsheet that outlines a baseline estimate of what the Big 12 gives up in future revenue in exchange for $960 million now ( a figure reported in the media). All numbers are in 000’s.

Column 1: Number of years

Column 2: Fiscal year ending

Column 3: Conference media revenue ($512 million for new contract)

Column 4: College Football Playoff Revenue ($12 million per team/year)

Column 5: Total media revenue

Column 6: Advance & Share of revenue paid to the financier

Column 7: Cumulative payment

I escalate the media contracts by 10% each year, or 60% for each six-year contract in the baseline projections. I run three additional scenarios: One with a 0% increase in media contract revenue, one with a 120% increase, and one with a 25% decrease each cycle.

Here are the key data points from each scenario:

Baseline (60% media contract increases each six-year cycle)

Big 12 pays $4.83 billion over 20 years for a $960 million advance

Financier earns a 17% return on the $960 million advance

No Increase in Media Contracts

Big 12 pays $2.78 billion over 20 years for a $960 million advance

Financier earns a 13% return on the advance

Media contracts increase 120% each cycle

Big 12 pays $7.58 billion over 20 years for a $960 million advance

Financier earns a 20.6% return on the advance

Media contracts decrease by 25% each cycle

Big 12 pays $2.14 billion over 20 years for a $960 million advance

Financier earns a 10.7% return on the advance

Final Thoughts

We may never know the key points of this type of deal. Because the Big 12 is a non-profit they can protect this deal from public record requests.

We won’t know:

Who scored the $20-$50 million brokerage fee to hook the deal.

If the financier inserted language that places the Big 12 and its members at risk if future media deals do not meet certain benchmarks.

The length of the deal and any provisions for extensions.

For these reasons, I believe these deals, crafted by conference employees under a cloak of secrecy are generally bad for college athletics. Look no further than Commissioner Larry Scott of the Pac-12 and his fatal deal to build a television network. Universities should make business cases individually, in public, and to their boards on financial matters such as this.

Just as interesting to most people, I think, would be the actual series of payments. How will this deal impact future revenue distributions per school? Will paying 20% to the PE group actually make school payouts decrease?

"Loan" or "Investment..." PE firms will have opinions on budgets, personnel, operations, etc., and that's when it will get really interesting for AD's and Presidents.